It can be a great way of taking advantage of low interest rates by investing in low duration bonds funds. These funds are usually designed to reduce volatility in bond price and have lower interest rate risks than most money markets funds. These funds invest only in debt instruments with maturities between six and twelve months. They also provide a steady stream of income. These types of investments are especially suitable for retired investors who are more cautious about taking on risk.

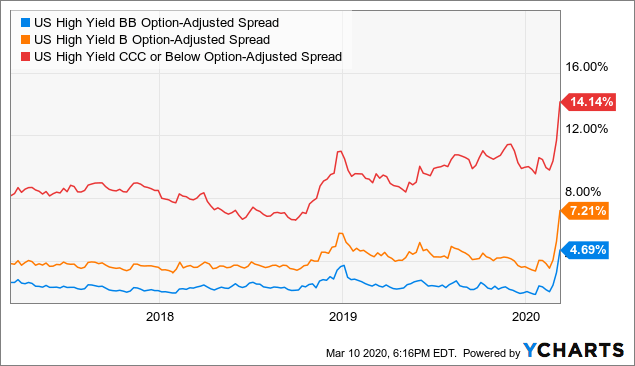

Many investors now measure interest rate risk by using duration. Duration is a term commonly used in fixed income investing, but some fund managers argue that too much focus on duration is lulling investors into a false sense of security. You should also consider other factors. For example, some bond funds may have short maturities, meaning that they will lose value significantly when interest rates rise. If interest rates were to rise two points, a bond with a tenure of eight years will lose 16 percent of their value. If the same bond were only for one year, however, the interest rate risk is much lower.

Duration is an indicator of your sensitivity to changes in interest rates. Some fund managers are looking to lower this sensitivity through the use derivatives and by purchasing bonds with shorter maturities. Some funds have placed duration limits on their prospectuses. Others have renamed their funds to emphasize the duration.

Pimco is a US-based bond giant that has recently added two low-deliverance funds to their offshore fund range. Mark Kiesel is responsible for the Pimco Low Duration, Global Investment Grade Credit funds. The other is the Pimco GIS Global Low Duration Real Return fund, run by Mihir Worah. Both funds invest in both corporate and government securities. Since inception they have had nearly equal NAV performances. The gap has narrowed over the years.

Investors who are concerned about rising interest rates may also consider the BLW fund. Its strong distribution yield makes it attractive for retirees. It has outperformed most bond indices over the past one year, and has outperformed S&P 500 during the past five-years. The fund's credit quality is poor, so it tends to underperform during downturns.

BLW's shorter duration can be a significant differentiator because it reduces the sensitivity of interest rate changes. For example, a bond of eight years duration would lose 16% if rates go up one point. A bond with a one-year duration would only lose 2 percent of its worth. Low maturity dates and credit quality can help to minimize interest rate exposure.

Many bond fund investors worry about the effects of rising rates. After the RBI cut key policy rate rates in April and a rise in yields on 10-year G secs, the yield has significantly increased. But, it is still quite a way from zero. Investors should therefore continue to watch the markets for signs of uncertainty.

FAQ

What's the difference between marketable and non-marketable securities?

The differences between non-marketable and marketable securities include lower liquidity, trading volumes, higher transaction costs, and lower trading volume. Marketable securities, on the other hand, are traded on exchanges and therefore have greater liquidity and trading volume. Because they trade 24/7, they offer better price discovery and liquidity. However, there are many exceptions to this rule. For instance, mutual funds may not be traded on public markets because they are only accessible to institutional investors.

Non-marketable securities can be more risky that marketable securities. They are generally lower yielding and require higher initial capital deposits. Marketable securities are generally safer and easier to deal with than non-marketable ones.

A bond issued by large corporations has a higher likelihood of being repaid than one issued by small businesses. The reason is that the former is likely to have a strong balance sheet while the latter may not.

Marketable securities are preferred by investment companies because they offer higher portfolio returns.

What is a bond?

A bond agreement between two people where money is transferred to purchase goods or services. Also known as a contract, it is also called a bond agreement.

A bond is normally written on paper and signed by both the parties. This document details the date, amount owed, interest rates, and other pertinent information.

When there are risks involved, like a company going bankrupt or a person breaking a promise, the bond is used.

Bonds are often combined with other types, such as mortgages. This means the borrower must repay the loan as well as any interest.

Bonds can also help raise money for major projects, such as the construction of roads and bridges or hospitals.

When a bond matures, it becomes due. This means that the bond owner gets the principal amount plus any interest.

Lenders can lose their money if they fail to pay back a bond.

What's the difference between a broker or a financial advisor?

Brokers specialize in helping people and businesses sell and buy stocks and other securities. They handle all paperwork.

Financial advisors can help you make informed decisions about your personal finances. They use their expertise to help clients plan for retirement, prepare for emergencies, and achieve financial goals.

Banks, insurance companies or other institutions might employ financial advisors. You can also find them working independently as professionals who charge a fee.

If you want to start a career in the financial services industry, you should consider taking classes in finance, accounting, and marketing. You'll also need to know about the different types of investments available.

Can bonds be traded

Yes, they are. Like shares, bonds can be traded on stock exchanges. They have been trading on exchanges for years.

They are different in that you can't buy bonds directly from the issuer. You must go through a broker who buys them on your behalf.

It is much easier to buy bonds because there are no intermediaries. You will need to find someone to purchase your bond if you wish to sell it.

There are several types of bonds. Different bonds pay different interest rates.

Some pay interest quarterly while others pay an annual rate. These differences make it easy to compare bonds against each other.

Bonds can be very useful for investing your money. You would get 0.75% interest annually if you invested PS10,000 in savings. If you invested this same amount in a 10-year government bond, you would receive 12.5% interest per year.

If you put all these investments into one portfolio, then your total return over ten-years would be higher using bond investment.

Statistics

- Individuals with very limited financial experience are either terrified by horror stories of average investors losing 50% of their portfolio value or are beguiled by "hot tips" that bear the promise of huge rewards but seldom pay off. (investopedia.com)

- For instance, an individual or entity that owns 100,000 shares of a company with one million outstanding shares would have a 10% ownership stake. (investopedia.com)

- Even if you find talent for trading stocks, allocating more than 10% of your portfolio to an individual stock can expose your savings to too much volatility. (nerdwallet.com)

- "If all of your money's in one stock, you could potentially lose 50% of it overnight," Moore says. (nerdwallet.com)

External Links

How To

How to create a trading plan

A trading plan helps you manage your money effectively. It allows you to understand how much money you have available and what your goals are.

Before setting up a trading plan, you should consider what you want to achieve. You may wish to save money, earn interest, or spend less. If you're saving money, you might decide to invest in shares or bonds. If you earn interest, you can put it in a savings account or get a house. You might also want to save money by going on vacation or buying yourself something nice.

Once you decide what you want to do, you'll need a starting point. It depends on where you live, and whether or not you have debts. It is also important to calculate how much you earn each week (or month). Your income is the net amount of money you make after paying taxes.

Next, you'll need to save enough money to cover your expenses. These expenses include rent, food, travel, bills and any other costs you may have to pay. Your monthly spending includes all these items.

Finally, you'll need to figure out how much you have left over at the end of the month. This is your net disposable income.

Now you've got everything you need to work out how to use your money most efficiently.

To get started with a basic trading strategy, you can download one from the Internet. Or ask someone who knows about investing to show you how to build one.

Here's an example of a simple Excel spreadsheet that you can open in Microsoft Excel.

This will show all of your income and expenses so far. You will notice that this includes your current balance in the bank and your investment portfolio.

And here's a second example. This was created by a financial advisor.

It will let you know how to calculate how much risk to take.

Remember, you can't predict the future. Instead, think about how you can make your money work for you today.